Retirement Tax Diagnostic™

See What the IRS Is on Track to Collect From Your Retirement

A 30-minute review of your projected lifetime tax bill and the biggest pressure points.

IRMAA, RMDs, the widow’s penalty, and the conversion windows you may be missing.

No cost. No obligation.

We will create a no-cost Retirement Tax Diagnostic™ so you can see your projected lifetime tax bill, your biggest tax “pressure points,” and what they could mean for your lifestyle and heirs.

The earlier you see the number, the more you can do about it. Each year that passes could narrow the options.

No cost. No obligation.

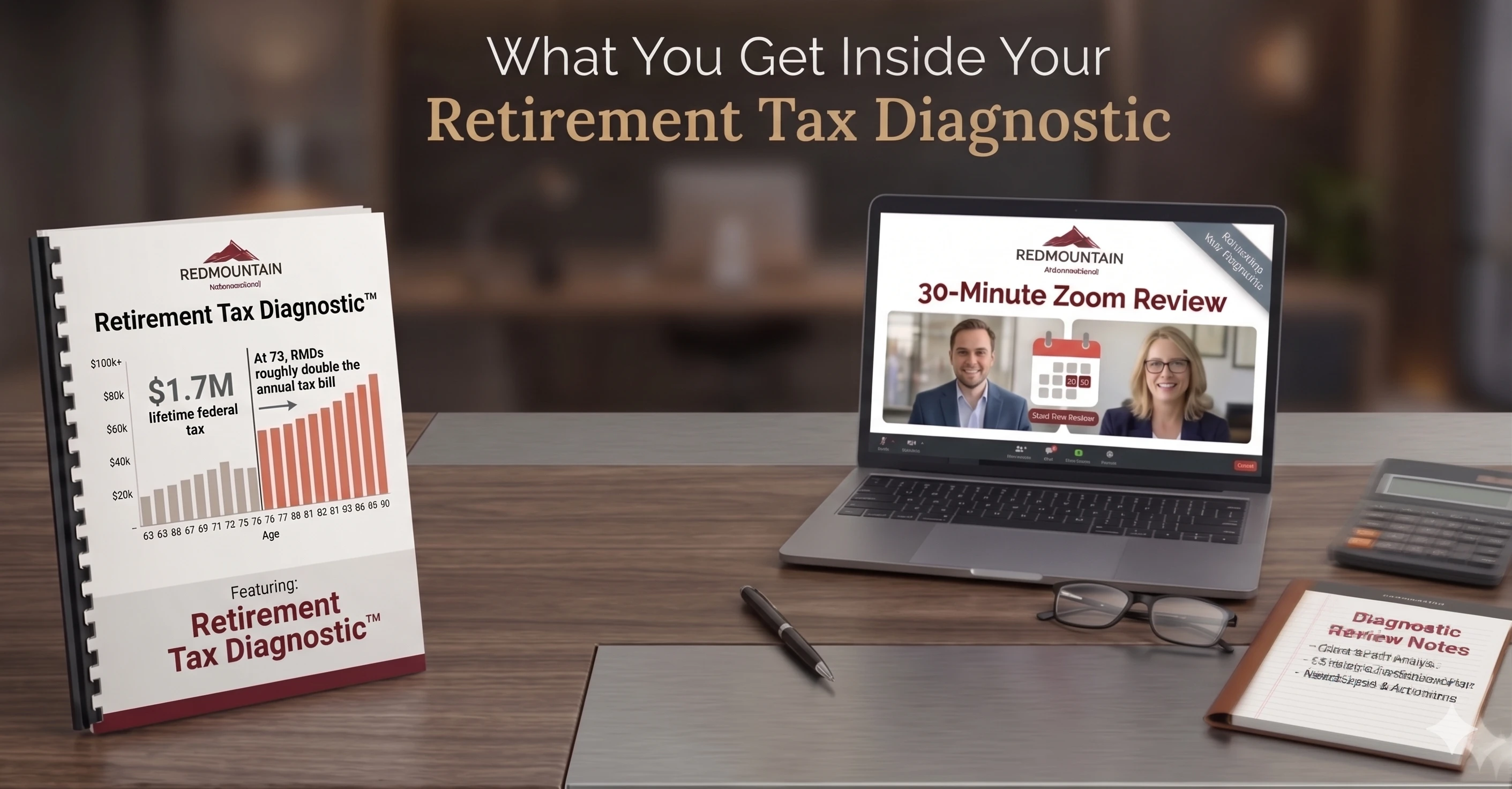

What You Get Inside Your Retirement Tax Diagnostic™

Your Lifetime Tax Diagnostic

- Projected lifetime federal income taxes based on your current path

- Estimated Medicare IRMAA surcharges (if any)

- A plain-English summary of your total expected tax bill if nothing changes

Your Biggest Tax “Pressure Points”

- Where forced IRA withdrawals (RMDs) could push you into higher brackets

- Where you may be exposed to IRMAA and the “widow(er)’s penalty”

- A simple explanation of what those spikes could mean for you and your spouse

30-Minute Zoom Review With Todd

- We review your Diagnostic together

- You see what you’re on track to pay and why

- At the end, if it makes sense, you can engage us to handle the planning and implementation for you

Who This Is (and Isn’t) For

This may be right for you if…

- You’re 55 or older, retired or within 10 years of retirement

- You’ve built up meaningful savings in IRAs, 401(k)s, or other retirement accounts

- You’re more concerned about not wasting money in taxes than “beating the market”

- You want clear numbers and plain English

This is not for you if…

- You’re looking for hot stock tips or day-trading ideas

- You don’t file U.S. tax returns or don’t plan to use a CPA/tax pro

- You just want a generic article or calculator, not a personalized analysis

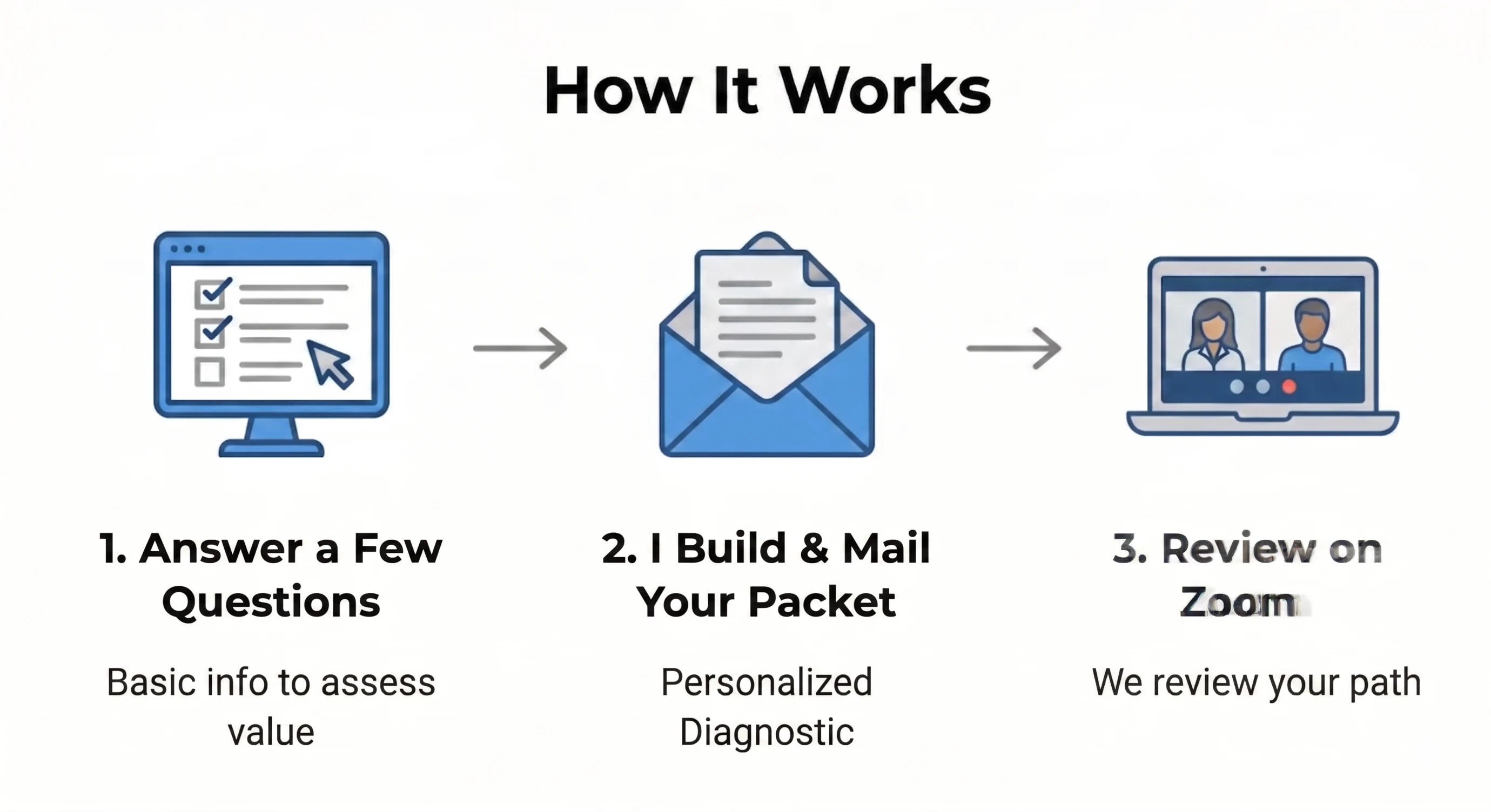

How It Works

Short get-acquainted phone call (~20 minutes)

- Basic info: age, retirement timing, account types, balances, etc.

- This helps me see if the Diagnostic may be valuable for you

I Build & Mail Your Diagnostic Packet

- Run a personalized Retirement Tax Diagnostic report

- Physically mailed to your address

We Review It Together on Zoom (30 minutes)

- We walk through the details, what it means, and answer your questions.

- At the end, if it makes sense, you can engage us to handle the planning and implementation for you as an advisory client.

A Note on Timing

A Diagnostic is most useful with runway — the years before year-end planning and required withdrawals begin, while there’s still room to act on what it shows.

I review each one personally, so I take on a limited number at a time. Right now I’m building new Diagnostics; closer to year-end, my attention shifts to the clients implementing the changes we find.

The Guarantee

Your Retirement Tax Diagnostic™ is yours to keep and use with any advisor or CPA you choose. I guarantee there will be no strings attached: if you decide not to work with us beyond this review, you still keep the full report and any materials at no cost.

This guarantee does not imply any investment results, tax outcomes, or market performance.

Who You’ll Be Meeting With

Todd Talbot, CFP®, ChFC®, CLU®

- CERTIFIED FINANCIAL PLANNER™ professional

- National Social Security Advisor certificate holder

- Certified Tax Specialist™

I run a planning-first advisory firm in Birmingham, Alabama, focused on helping affluent retirees keep more of what they’ve saved and send less to the IRS over their lifetime. I’m here to put real numbers in front of you, in plain English, to help you make informed decisions about your retirement taxes.

Frequently Asked Questions

Q: What does “no cost” really mean?

There is no fee for the Retirement Tax Diagnostic or the 30-minute review. If you decide you want ongoing planning and an advisory relationship afterward, those services do have fees, which I’ll explain clearly before you decide.

Q: Do you guarantee tax savings?

No. This is a tool to help you understand what could be one of your biggest expenses during retirement… taxes. It uses assumptions that may change over time. I don’t guarantee specific tax savings or investment performance. I do believe you’ll understand your projected tax path better.

Ready to See What the IRS Is On Track to Collect From Your Retirement?

Request your no-cost Retirement Tax Diagnostic™ and get a clear view of your projected lifetime tax bill and your biggest tax pressure points.